What Is a Prepaid Solar Lease? Colorado Homeowner's Guide (2026)

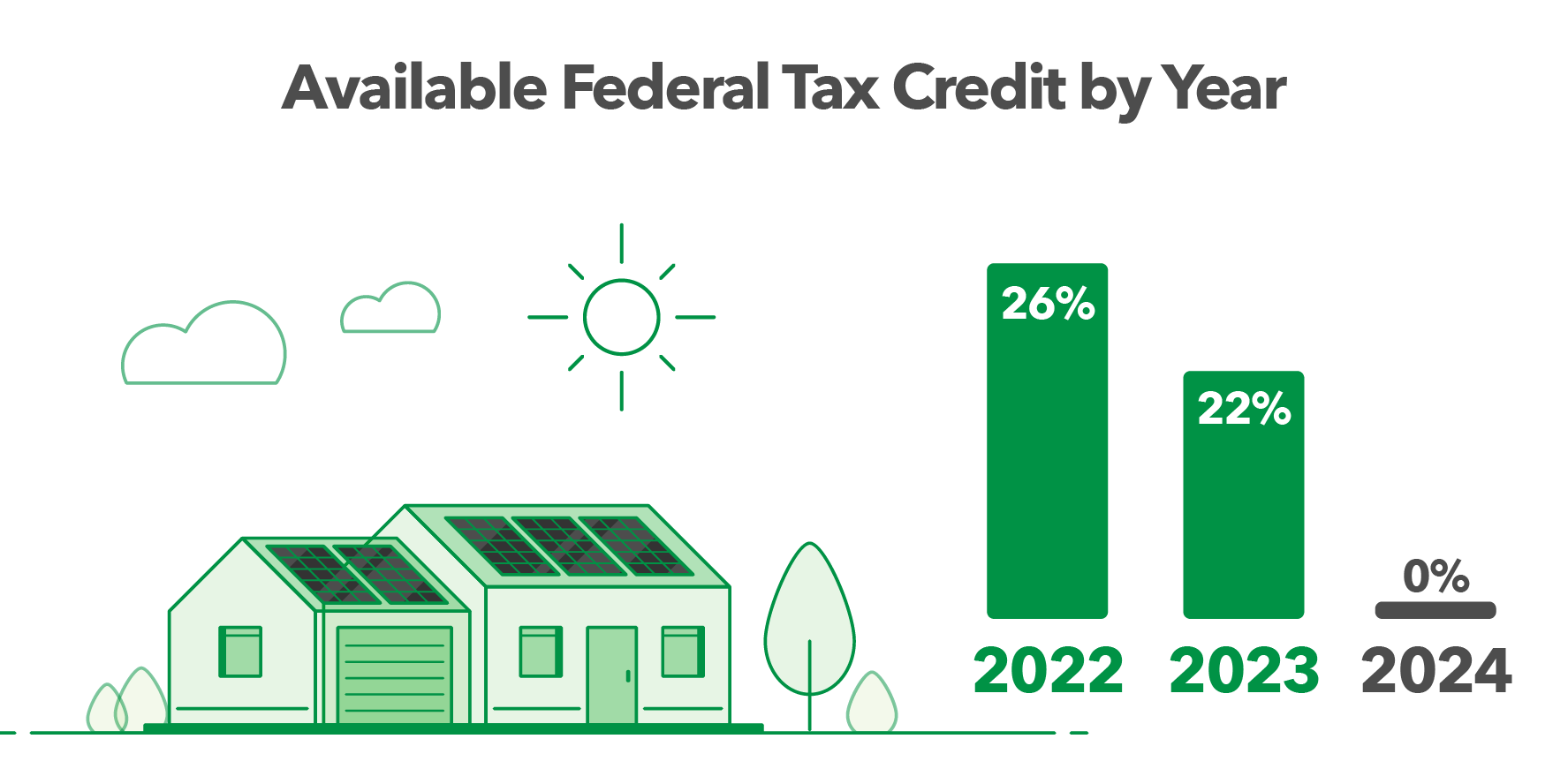

The federal residential solar tax credit that Colorado homeowners relied on for years expired at the end of 2025. If you've been putting off going solar — or have been quoted prices that now look different — you're not alone. The financing landscape changed. But a new model has stepped in to fill the gap, and it's more accessible than most homeowners expect.

It's called a prepaid solar lease. It's not a traditional lease, not a loan, and not a cash purchase — but it borrows elements from all three. This guide explains exactly how it works, what the pros and cons are, how it compares to other financing options, and what Colorado homeowners specifically need to know before signing anything.

Why the Prepaid Solar Lease Emerged in 2026

For over a decade, the Section 25D residential Investment Tax Credit (ITC) let homeowners claim 30% of their solar system cost as a federal tax credit. That program ended for residential installations on January 1, 2026.

What didn't end is the commercial solar tax credit — Section 48/48E. This credit applies to solar systems owned by businesses and corporations, and it remains in place. A prepaid solar lease is built around exactly that distinction: a business entity owns the rooftop solar system during an initial holding period, claims the commercial ITC, and passes that value through to the homeowner in the form of a lower upfront price.

The result is a financing path that lets you benefit from federal tax incentive value — even though you can no longer claim it directly as a homeowner.

What Is a Prepaid Solar Lease? (Plain-Language Definition)

A prepaid solar lease is a solar financing arrangement where:

- A third-party entity (usually a special-purpose investment vehicle) owns the solar system installed on your roof for a defined holding period — typically 5 to 8 years

- The third party claims the Section 48 commercial tax credit on the system

- That credit value is passed to you as a discount baked into your financing terms

- You make no monthly lease payments — the "lease" is prepaid (usually funded via a loan product) at the time of installation

- At the end of the holding period, full ownership of the system transfers to you

The term "prepaid lease" can be confusing because it sounds like you're leasing something indefinitely. You're not. The lease structure is a legal mechanism to enable the third-party tax credit claim. The end result — after the holding period — is that you own the system outright.

How a Prepaid Solar Lease Works: Step by Step

Here's what actually happens from installation to full ownership:

- You qualify for financing. The financing entity reviews your credit and property eligibility — similar to a standard solar loan process.

- A third-party business entity purchases the system. That entity — not you — becomes the legal owner of the panels installed on your roof.

- The third party claims the Section 48 commercial ITC. This reduces their tax liability and creates the economic value that gets passed through to you.

- You make monthly loan payments on a fixed-term loan. The loan amount already reflects the ITC value — that discount is baked in at origination. Payments are fixed; there are no escalators.

- You use the energy your panels produce. Net metering through Xcel Energy credits your utility bill for excess generation, just like any other solar system.

- At year 5 (or 6.5 or 8, depending on the product), ownership transfers to you. This is a contractual right, not an option the financing entity can walk back. After transfer, you own the system free and clear.

The key distinction from a standard lease: you're not paying for electricity production. You're paying back a loan. The "lease" wrapper is a legal and tax structure, not an ongoing tenancy arrangement.

Pros of a Prepaid Solar Lease

Access to Federal Tax Incentive Value Without Owing Federal Taxes

The most significant benefit: Colorado homeowners who pay little or no federal income tax — retirees, small business owners with deductions, or anyone in a low-tax-liability year — couldn't fully utilize the old residential ITC anyway. The prepaid lease monetizes that tax credit through a business entity that can fully use it, then passes the value to you through lower pricing.

No Large Upfront Cash Requirement

Unlike a cash purchase, you're not writing a check for $20,000–$40,000 at signing. The prepaid lease/loan structure spreads cost over time with fixed monthly payments. For most Colorado homeowners, those payments are at or below their current Xcel Energy bill.

No Monthly Lease Volatility

Traditional solar leases often include annual payment escalators of 1–3% per year. Prepaid lease structures — done correctly — lock in fixed payments with no escalators. Your monthly obligation stays the same for the life of the loan.

You End Up Owning the System

After the holding period, you own the panels, inverters, and all equipment. The system becomes a permanent part of your home's value. This is fundamentally different from a traditional lease, where you never own the system and must either extend the lease, buy out at potentially inflated prices, or have panels removed at end of term.

Stackable with Colorado State Incentives

The prepaid lease doesn't preclude Colorado-specific incentives. The Colorado DR 1307 income tax credit — available for qualifying solar and battery storage systems — can still apply for eligible homeowners. Xcel Energy's net metering program applies normally, crediting your bill for excess production at near-retail rates. If you or someone in your household qualifies for Xcel's PSPS (Portable Solar Power System) Medical Rebate, that can also be explored in the same conversation.

Cons and Risks to Understand

Home Sale Complexity During the Holding Period

While the third-party entity owns the system, there will typically be a UCC lien or equivalent instrument recorded against your property. If you sell your home before the holding period ends — typically before year 5 — you'll need to coordinate with the financing entity to either transfer the agreement to the new buyer or pay off the remaining obligation. This is manageable, but it requires advance planning. Disclose it to your real estate agent early.

You Depend on the Third Party's Financial Stability

During the holding period, the third-party entity is the legal owner of your solar equipment. If that entity became insolvent, the ownership transfer could be complicated — even if your contractual right is well-documented. This is why the financial backing and legal structure of the financing entity matters enormously. Not all prepaid lease products are created equal.

ITC Eligibility Risk in Some Products

The Section 48 commercial credit is not automatically available just because a business entity holds the system. The IRS has specific requirements about what qualifies as "active management" of the asset, and some prepaid lease structures in the market are facing legal challenges on exactly this question. If the commercial ITC claim is later disallowed, the economics of the deal change — and homeowners should understand who bears that risk in the contract.

Long-Term Savings vs. Cash Purchase

A cash purchase with no financing costs will almost always produce better 25-year economics than any financed option — prepaid lease included. The prepaid lease is the right tool when a cash purchase isn't feasible or desirable, not an upgrade over paying cash.

Prepaid Lease vs. Loan vs. Cash Purchase: Side-by-Side

| Prepaid Lease | Solar Loan | Cash Purchase | |

|---|---|---|---|

| Who owns the system? | Third party → transfers to you after 5–8 years | You (from day 1) | You (from day 1) |

| Federal tax credit benefit? | Yes — via third party's commercial ITC, passed through as discount | No (residential ITC expired 2025) | No (residential ITC expired 2025) |

| Monthly payments? | Fixed loan payments, no escalators | Fixed loan payments | None after purchase |

| Upfront cost | Low | Low | High ($20K–$40K+) |

| Home sale complexity | Moderate (UCC lien during holding period) | Low (loan payoff at closing, like a HELOC) | Low (system conveys with home) |

| Long-term savings | Good | Good | Best |

| Who manages maintenance? | Third party during holding period; you after transfer | You (with installer warranty) | You (with installer warranty) |

Colorado-Specific Context: What You Should Know

Colorado DR 1307 Income Tax Credit

Colorado's DR 1307 provides a state income tax credit for qualifying solar and battery storage systems. This credit applies at the state level and is separate from the now-expired federal residential credit. For eligible homeowners, it can be stacked with a prepaid lease structure, since it relates to the installation at your property rather than ownership. Verify eligibility with a Colorado tax professional.

Xcel Energy Net Metering

If you're in Xcel Energy's service territory — which covers most of the Denver metro, including Lakewood, Littleton, Arvada, Golden, and surrounding areas — your solar system qualifies for net metering. Under Xcel's current program, excess solar generation credits your bill at near-retail rates. That means your panels produce value even when your usage doesn't match your production. A prepaid lease does not affect your ability to net meter — the energy produced by your system is still yours.

PSPS Medical Rebate

Xcel Energy's PSPS (Portable Solar Power System) Medical Rebate offers up to $10,000 for qualifying customers with documented medical needs for continuous power. If you or a household member relies on powered medical equipment, this is worth exploring alongside any solar installation — including a prepaid lease.

Denver Metro Installer Landscape

The prepaid lease market in Colorado is still developing. Not every installer in the Denver metro area offers well-structured products, and the quality of due diligence on the financing entity varies significantly. Colorado homeowners should be especially cautious of products that can't produce independent legal documentation of their commercial ITC eligibility.

Is a Prepaid Solar Lease Right for You?

A prepaid solar lease tends to be the strongest fit for Colorado homeowners who:

- Don't have $25,000–$45,000 in cash to purchase outright but want to benefit from incentive value that's no longer available through direct ownership

- Have limited federal tax liability — retirees, business owners with significant deductions, or anyone who couldn't have fully used the old residential ITC anyway

- Plan to stay in their home for at least 5–7 years, giving the holding period time to resolve before any potential sale

- Want to own the system eventually — not rent power indefinitely through a traditional PPA

- Are comfortable with the third-party ownership structure during the holding period, given proper vetting of the financing entity

A prepaid lease is not the right fit if you're planning to sell in the next 2–3 years, if you have cash available and the discipline to deploy it, or if you're not comfortable with any complexity in a potential future real estate transaction.

How Concert Finance's Propel Product Works (What Solar Wave Offers)

Solar Wave is completing the approval process to offer Concert Finance's Propel Energy Services Agreement (ESA) — one of the more rigorously structured prepaid lease products available in 2026.

Under a Propel agreement:

- A third-party entity owns the system for the first five years, with options at 6.5 or 8 years

- That entity claims the Section 48/48E commercial tax credit

- The credit value is passed to the homeowner as a reduction baked into a fixed 25-year loan originated through Medallion Bank

- Ownership transfers to the homeowner at the contractual date — this is a binding right, not an option the financing entity can defer

- No monthly lease payments — the structure is loan-based with fixed terms

- No escalators — your payment doesn't increase year over year

Solar Wave evaluated several prepaid lease products before selecting Propel. The determining factors were the quality of the commercial ITC legal documentation, the financial backing of the entity structure, and the clarity of the ownership transfer terms. When Propel becomes available for Colorado installations, it will be Solar Wave's primary third-party ownership option.

Questions to Ask Any Solar Company Offering a Prepaid Lease

As prepaid leases grow in popularity, the number of variations in the market grows too. Before signing anything, Colorado homeowners should ask:

1. Has the commercial ITC eligibility been confirmed by independent tax counsel?

The Section 48 commercial credit is not automatic. Some products in the market are facing active legal challenges. Ask for documentation showing the structure was reviewed and validated by qualified, independent tax attorneys — not just the financing company's internal team.

2. Who is the third-party entity, and what is their financial standing?

Understand who owns your panels during the holding period. How long have they been operating? What happens to the ownership transfer if they face financial difficulties? Are there contractual protections built in?

3. Is the ownership transfer a binding contractual right?

The transfer at year 5 (or the agreed date) should be a hard contractual right — not something the entity can defer, renegotiate, or convert to a buyout requirement at inflated prices. Review this language directly in the agreement before signing.

4. How does a home sale work during the holding period?

There will typically be a UCC filing against your property. Understand the exact process — and the timeline — for resolving that in a real estate transaction, so it doesn't surface as a surprise at closing.

5. Who handles monitoring, maintenance, and equipment issues during the holding period?

IRS requirements for commercial credit typically require the third-party owner to actively manage the system. Confirm this is in writing, and understand the service request and response process for any equipment issues during the years before transfer.

The Bottom Line

The prepaid lease is a legitimate, thoughtfully engineered response to the expiration of the residential ITC. For Colorado homeowners who want to own their system, capture as much federal incentive value as possible in 2026, and do it without a large upfront cash investment — a well-structured prepaid lease is the strongest option currently available.

The phrase "well-structured" is doing real work in that sentence. The difference between a prepaid lease product that delivers on its promise and one that doesn't comes down to the quality of the legal structure, the financial stability of the holding entity, and the clarity of the ownership transfer terms. That's the due diligence Solar Wave applied when evaluating products — and it's the standard we'd encourage any Colorado homeowner to apply.

If you'd like a no-pressure conversation about whether a prepaid lease makes sense for your home, what the numbers look like for your specific energy usage, and how it stacks against a loan or cash purchase — request a free proposal from Solar Wave. No commission reps. No high-pressure tactics. Just honest numbers.